‘Barbell Pricing’ is a Heavy Lift for Brands in a K-Shaped 2026

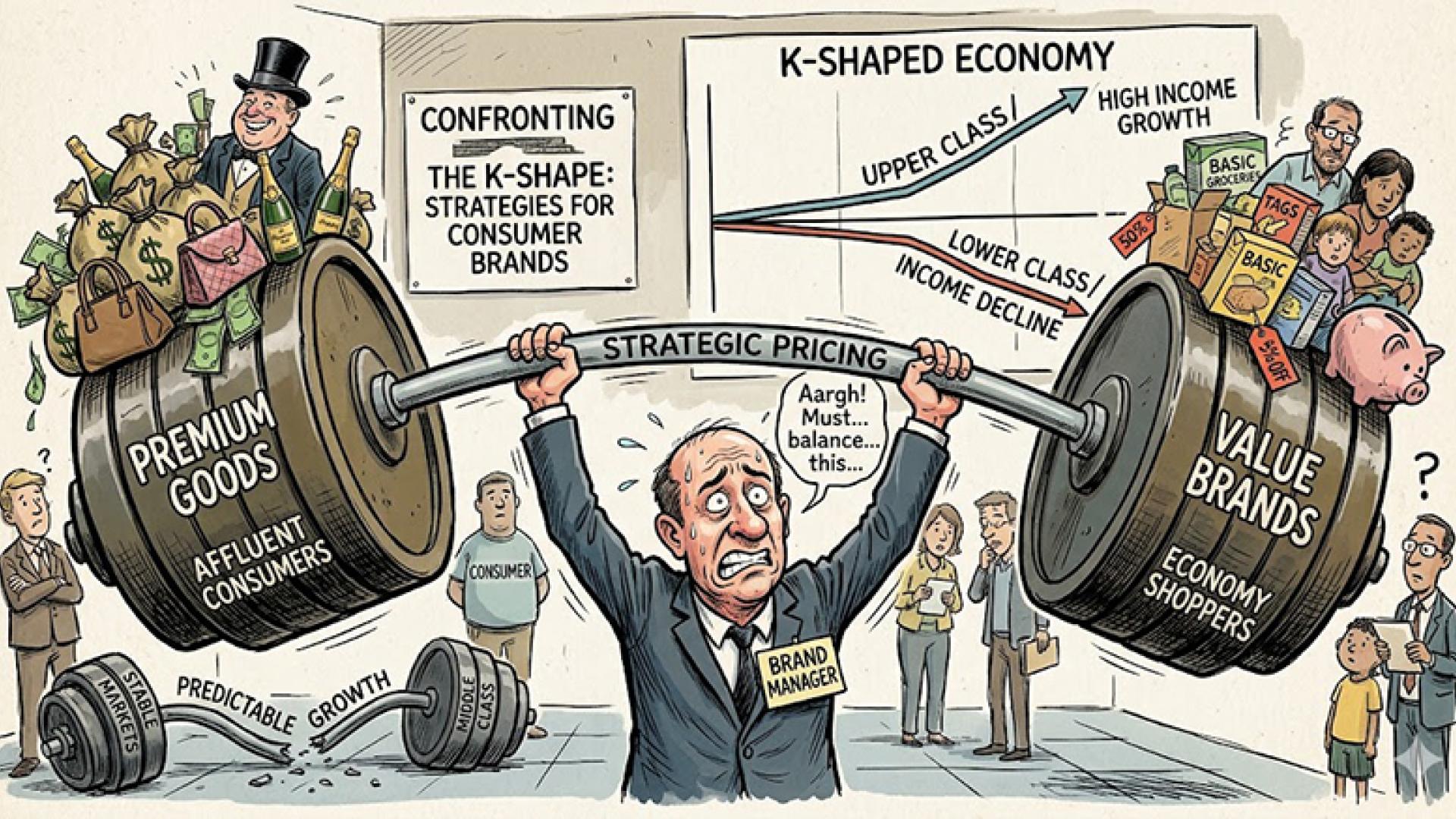

SIX YEARS AFTER behavioral economist Peter Atwater coined the term “K-shaped economy,” the metaphor has become the defining structural reality for the CPG industry.

The upper arm of the K consists of thrivers—households with soaring assets who are keeping the economy afloat. The lower arm consists of strugglers—wage earners and a shrinking middle class being pulled downward by the persistent cost of essentials.

Data from Moody’s Analytics highlights the stakes: the top 20% of households are now responsible for nearly 60% of all consumer spending. For CPG companies, the implication is clear: the middle has evaporated. Success in 2026 requires a double-ended “barbell” strategy that captures both the splurge-ready thriver and the budget-constrained struggler.

Brands Move Beyond Price-Led Growth

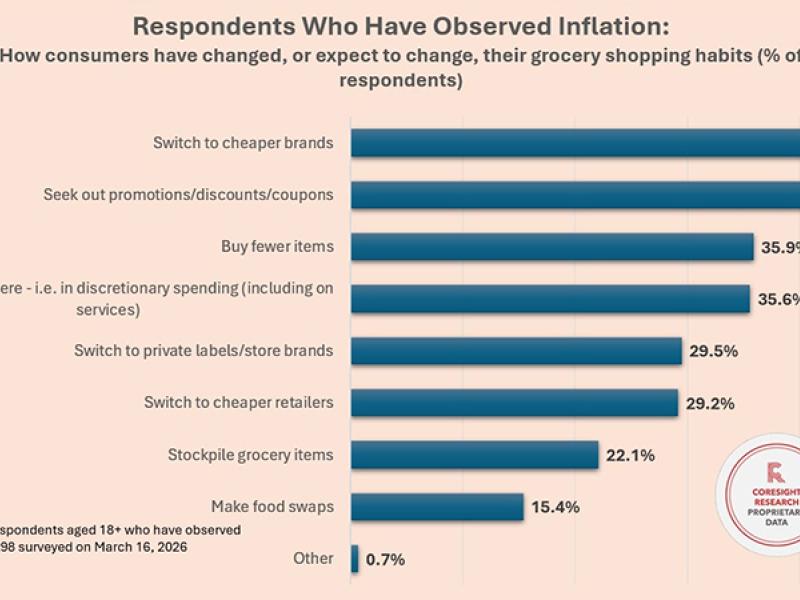

During a recent FMI webinar, Steve Markenson, VP of Research at FMI, and Jack O’Leary, Director of eCommerce Strategic Insights at NielsenIQ, noted that while inflation has slowed, its cumulative effect remains the primary driver of behavior. O’Leary observed that strugglers are experiencing persistent, above-average inflation on the staple categories they need most.

O’Leary discussed how prices have trended for a typical basket of widely-purchased household staples: “When we look at this over this period, you see numbers of these items are growing at an annualized rate of over 10%. And the total basket, albeit a small one here, grew at an 8.6% rate over these years here. That's substantially more than 4.5% [CPI rate]”

For CPG manufacturers, this has created a dangerous volume trap. Over the last two years, many brands reported healthy revenue growth driven entirely by price hikes, while actual unit volume remained flat or negative.

Economists have noted that in 2026, the price ceiling has been reached. To reignite unit growth, brands are abandoning one-size-fits-all models in favor of sophisticated Price Pack Architecture (PPA) and digital personalization that addresses the distinct needs of each arm of the K.

Brands that rely on broad consumer appeal are feeling the weight at both ends of the economic barbell. They are pursuing parallel strategies across the five Ps.

1. Product: Functional Premiumization vs. Value Simplification

CPG brands are splitting their R&D pipelines to address two entirely different consumer psychology profiles.

- Thrivers: Brands are stacking high-value attributes to justify premium pricing. We see a surge in GLP-1 companion foods—high fiber and protein—and clean-label supplements. Brands have moved beyond basic nutrition to offer specific metabolic-support benefits tailored to affluent, health-conscious consumers who view food as medicine. This cohort is willing to pay more for "proof of efficacy" and "ingredient purity."

- Strugglers: CPGs are launching back-to-basics lines. These stick to core, high-velocity versions of products that prioritize satiation and reliability over complex flavors. In the supplement space, the trend is moving away from expensive all-in-one multivitamins toward single-ingredient solutions. This allows consumers to build a regimen based on monthly affordability, rather than committing to a high-cost bundle they cannot maintain.

2. Price: Surgical Rollbacks and The Private Label Threat

Pricing in 2026 is no longer a blunt instrument used for across-the-board increases.

- Tactical Rollbacks: Major players including PepsiCo and General Mills have implemented price cuts of up to 15% on specific snack lines. These are not broad concessions but surgical strikes designed to win back low-income shoppers who migrated to private labels.

- The Private Label Paradox: Private brand dominance is now cross-demographic. High-income thrivers are increasingly shopping value banners like Aldi and Costco for staples to preserve capital for high-end splurges. To compete, national brands seek to prove unique utility—investing in R&D that provides a functional benefit, such as superior shelf-life or advanced muscle health, that a store brand cannot easily replicate.

3. Packaging: Engineering for the Budget and the Lifestyle

Packaging is the most visible tool in a CPG's PPA toolkit to bridge the economic gap.

- Entry-Point Packaging: To keep strugglers in the brand family, CPGs are introducing trial sizes or $1.99 opening price point packs. This keeps the brand in the basket when the standard family size becomes a liquidity hurdle. As recent as last fall Coca-Cola began adjusting its lineup accordingly. Its chief operating officer, Henrique Braun, talked to analysts during a fall conference call about the divergency the company was seeing in spending between income groups. He noted that Coca Cola is pursuing the premiumization and affordability angles as it looks to sell more of its higher end brands while seeking new options such as mini cans for those consumers looking to still indulge in the brand but spend less.

- Bulk Efficiency: For thrivers, the focus is on club-sized pantry stock. These shoppers have the capital to buy 70-count laundry pods or bulk supplement jars, securing a lower price per unit through a high upfront investment that lower-income earners simply cannot bridge.

- Packaging as Social Currency: Premium beverages and snacks are using high-design, expressive packaging that acts as a status symbol for the upper arm, effectively turning a simple drink into a lifestyle accessory.

4. Promotion: Trade Spend Optimization vs. Agentic Discovery

CPG brands are overhauling how they allocate their promotional budgets to move units in a bifurcated market.

- Trade Spend for Volume: For the lower arm, promotions are shifting from percentage-off deals to "hard" price-point guarantees (e.g., "Must-buy 2 for $5"). This helps price-sensitive shoppers calculate their exact spend before reaching the register. Brands are focusing trade spend on high-velocity staples to defend market share against aggressive private label pricing.

- AI and the Convenience Loop: Thrivers are early adopters of agentic commerce—using AI agents to manage shopping lists and automated replenishment. For CPGs, this means your digital shelf presence is now about structured data. If your product isn't machine-readable for specific dietary or lifestyle prompts, the AI agent will skip you in favor of a competitor or a premium private label. Promotions for this group focus on experience-led content and exclusive early access to new innovations.

5. Placement: The Omni-Channel Shift

The 2026 shopper is "channel-agnostic."

- Channel Cross-Pollination: High-income thrivers are increasingly found in value channels for staples. Brands are responding by placing "Premium" tiers (organic or high-protein versions) in these discount stores to capture the "Thriver" who is bargain-hunting.

- Digital Transparency: Brands are prioritizing placement on platforms that feature a "running total" in the digital cart. This allows strugglers to manage their spending in real-time, preventing the "sticker shock" that leads to abandoned carts or items being left at the physical checkout.

The 2026 Mandate

The K-shaped economy forces CPG companies to be better at precision. The center of gravity has moved. To thrive, brands must de-average their sales data and recognize that their portfolios are in fact barbell-shaped.

By protecting the base with value-engineered staples and driving margin through attribute-heavy premiumization, CPG leaders can navigate the divide. In this environment, the most dangerous place to be is stuck in the middle.

The Execution Gap

A Q&A with Ellen Kan, Partner at Simon-Kucher

As brands navigate the K-shaped reality of 2026, the distance between “strategy” and “shelf” has never been wider. We sat down with Ellen Kan, a Partner in the Consumer practice at global pricing consultancy Simon-Kucher, to discuss how brands can manage the complexity of a barbell portfolio without eroding their margins.

CPGM: We see many brands attempting to 'barbell' their portfolios—investing in super-premium and extreme-value simultaneously. Is the operational complexity of managing both ends of the 'K' worth the risk?

Ellen Kan: Yes, a barbell strategy is critical to managing profitability right now, but there is real margin risk if it's executed poorly. SKU proliferation without a disciplined architecture can drive massive supply chain and shelf complexity. The most successful companies ensure every SKU has a clearly defined 'job to be done.' This requires sharpening focus and managing the portfolio with discipline—rationalizing underperforming items even as you add SKUs to address white space.

CPGM: Analysts are watching the middle-income cohort with a laser focus. What 'canary in the coal mine' behaviors are you seeing in middle-class data right now?

Ellen Kan: We are seeing more deal-seeking behavior and promotion sensitivity; consumers are waiting to buy their preferred brands only when they are on sale. Trip frequency has also consolidated into fewer, larger trips, often within value-oriented channels like mass and club. The real risk is structural: in categories where the perceived value gap between private label and branded goods has shrunk, we see increased trial of private label. If shoppers learn that private label is 'good enough,' that trade-down becomes permanent.

CPGM: How can CPGs justify R&D spend for innovation when the downward arm of the K is so price-sensitive?

Ellen Kan: Innovation must deliver a real, measurable benefit to succeed in 2026—this means fewer, bigger bets instead of undifferentiated line extensions. In ‘Small Luxuries' like snacks or beverages, that means real functional attributes or emotional benefits. In 'Big Staples' like laundry or paper, the benefit must come from delivering cost or time efficiency through format innovation. As stress on wallets grows, consumers are more likely to trade off convenience while preserving their small indulgences.

- Interview by Carol Radice