CPG Manufacturers Face a Challenging Year

CONTINUED PERCEPTIONS of a challenging economy are combining with persistent inflationary pressures to discourage U.S. consumers at the grocery store, prompting leading CPG manufacturers to continue to report volume declines. In fact, manufacturers and retailers should be preparing for an extended period of depressed volume, according to a recent report by Cadent consultants.

Despite some moderation of food-price inflation and higher expectations for the performance of the overall economy under a re-elected President Trump, American consumers continue to feel squeezed at the supermarket checkout. The key to giving shoppers relief, Cadent’s research found, is increasing trade promotion.

Entering 2025, Cadent predicted that CPG manufacturers and retailers will be contending with four primary market forces: consumer cost sensitivity, retailer efforts, private label growth and an increase in marketing-spending mediums.

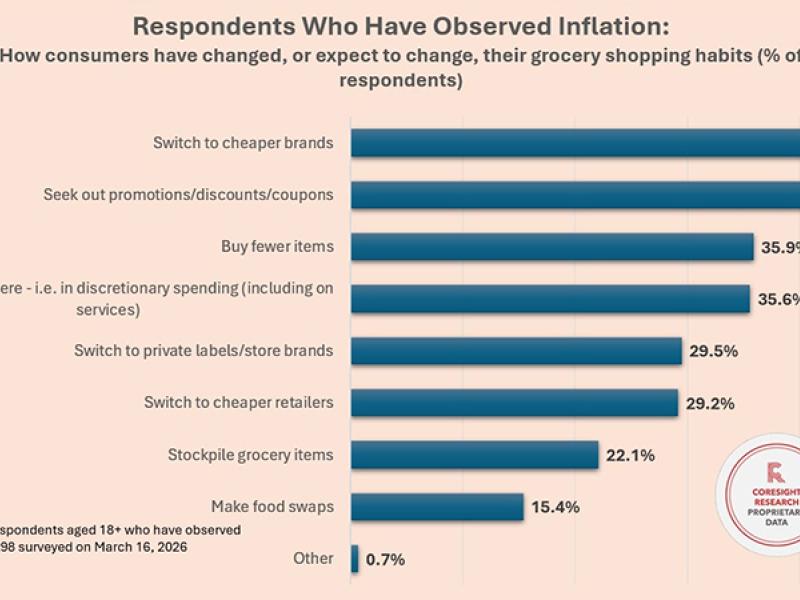

Well-documented rising costs have led to reduced real income for U.S. consumers over the last few years, compelling them to pull back on spending and protecting their budgets. More than 56% of consumers experienced pricing pressures for foods and beverages in 2024, making that category the most stressful for them compared with two years earlier; gas and transportation costs pressured 49% of Americans, and rent and housing costs concerned 47%, Cadent found. At one point in 2024, another survey, this one by CNBC, showed 54% of young Americans saying food costs were the biggest strain on their finances.

The fact that Democratic presidential candidate Kamala Harris believed she could score political points by eagerly alleging—with no evidence—that the food industry was engaged in price fixing underscored the anxieties American consumers have been feeling.

Retailers have been doing their share to prop up volume with major initiatives to lure back shoppers. Recently, for example, Walmart rolled back prices on nearly 7,000 items, and Target cut prices on more than 1,500 items. All supermarket retailers are aggressively reducing prices to maintain customer loyalty and incentivize more robust purchasing across the store, Cadent noted.

Meanwhile, the increasing presence of private label products is drawing consumers away from traditional brands and toward new offerings and new retailers, the consulting firm said.

CPG brands are fighting back to revive volumes as well. They’re optimistic that they can find new growth outside of pricing, with product innovation in the spotlight, Cadent said. Over the past several years, many brand portfolios “had become bloated, riding the tailwinds of a strong decade plus” of consumer sales with relatively little inflation.

Marketing spending is rapidly accelerating as these volume pressures rise. After 2023 saw the revival of marketing spending, 2024 added fuel to the fire, with increasing dollar sales—along with a higher spend as a percentage of sales—lifting actual spending by $33 billion since 2022 – a 17% increase. In 2025, CPG manufacturers don’t anticipate a pull-back, with marketing spending expected to reach 20% of total sales, nearly reaching historically high 2012 levels.

Still, manufacturers ranked product innovation as the No. 1 most impactful area for driving volume growth in 2025, the firm said. And despite tight wallets, 47% of all shoppers said they will often purchase new, interesting grocery items that they see. With heavy supply-chain constraints and shifting consumer preferences, brands critically assessed what mattered most, and M&A activity narrowed its focus to singular, high-performance brands, Cadent said.

Beyond innovation, manufacturers are relying on brand marketing, channel expansion and trade promotion to lift volume growth in the year ahead. For many brands, the next several years will be an exercise in gaining market share, rather than holding on to a piece of an ever-growing pie. While pricing tactics will play a role, equity-building levers must also be employed, Cadent projected.