As Customers Shop Harder, How Will Brands Respond?

INFLATION AND HIGH GAS PRICES aren't the only things making grocery bills expensive. Tariffs and broader macro pressures are altering consumer behavior in structural, possibly enduring ways.

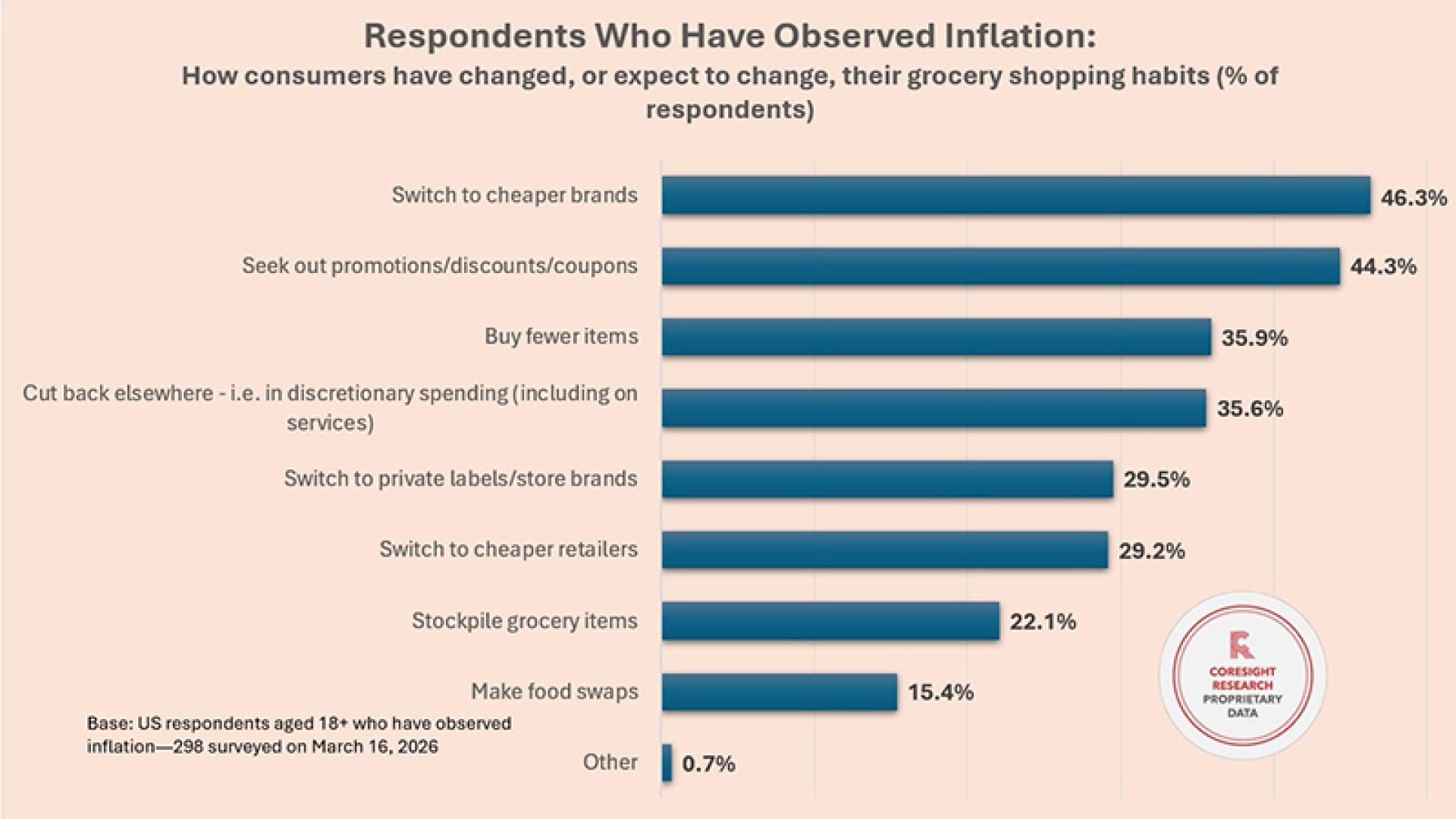

A new report on consumer grocery shopping habits from Coresight Research found consumers are visiting grocery stores more often but spending less time there. Feeling the affordability squeeze, 46.3% of consumers surveyed said they have switched to cheaper brands, 44.3% are couponing more, and 35.9% are simply buying less.

In its report, How US Consumers Are Shopping for Groceries: Prioritizing Value, Convenience and Private Labels Amid Macroeconomic Pressures, Coresight analysts unpack a range of shopper responses to the rising costs of groceries. While some choices are momentary and pragmatic, others may be signals of longer-lasting changes. For CPG brands, this presents some difficult strategic choices.

“Shoppers are becoming more deliberate in how they allocate spend across channels, trips and baskets, while staying highly responsive to prices and promotions,” say the study authors. “Despite this, underlying demand remains subdued, with weak unit growth signaling continued pressure on consumption.”

The report breaks down four fundamental behaviors of concern to brand marketers:

- Bargain hunting through more frequent, lower-volume visits.

- Decline in unit sales, as shoppers limit spending

- Price-awareness amid expectations of future increases

- Switch to lower-priced brands and private labels

These factors may put some mainstream brands or pack sizes at risk, and lead grocery retailers to reexamine assortments, the study suggests. So-called SKU-rationalization has always presented potential perils for brands on the bubble, while the introduction of newer, AI-enabled decision-making tools could alter the calculus in fundamental ways.

Waging The Assortment Battle

We put some questions to Coresight analyst Sujeet Naik, who offered some advice for brands to defend their shelf space.

“Absolutely fight, but fight smart,” he said. “Retailers are likely to become even more disciplined around assortment productivity over the next 12–18 months. Slower unit growth, rising supply-chain costs and increased focus on inventory efficiency all point toward SKU rationalization, especially in crowded categories.”

The key question, he maintains, is how. “Volume alone is not enough anymore. Retailers want SKUs that solve a problem: value SKUs that anchor their price credibility, premium SKUs that drive basket size, or an innovation that generates trial and traffic.”

“Brands should be working closely with their retail partners now to understand where the rationalization pressure is highest and positioning their portfolio accordingly. If you have SKUs that are marginal on velocity, it may actually be better to sunset them yourself before the retailer does it for you.”

Tougher Going for Nonfoods

Notably, the Coresight unit sales findings indicate that consumer value-seeking behavior may be more intense for nonfood grocery categories. Nonfood unit sales were down 3.0 percent and 2.8 percent for the four weeks ended Feb. 22 and Mar. 22, the report says. Food unit sales were down 1.8 percent and 0.1 percent in the same periods.

“In many categories, it increasingly looks like consumers are reaching resistance levels on pricing in nonfood grocery,” Naik said. “Household goods, health and beauty and general merchandise have absorbed multiple rounds of price increases over the past few years, and shoppers are now responding by delaying purchases, buying fewer units or switching channels.”

One implication is a potential loss of volume if consumers find that using less or buying less often doesn't significantly impact their lives. As a result, future growth will become much harder to achieve through pricing alone, he added. “Brands and retailers may need to shift back toward driving volume rather than relying on price/mix to support sales growth.”

Flight to Value Brands

The study also noted that consumers’ shift to value includes lower priced brands recently, perhaps more than private label. Is it time to adjust competitive strategy?

Said Naik, “What we are seeing is not necessarily a rejection of private label, but a more selective and pragmatic consumer. Consumers are looking for value wherever they can find it, and they are increasingly open to national brands that are competing harder on price and promotion.”

He suggested that the competitive strategy adjustment needed is less about repositioning and more about doubling down on the fundamentals: Make sure your price-pack architecture offers an accessible entry point. Keep your promotional calendar tight. Invest in the innovation that reminds consumers why they preferred you in the first place.

Four Go-To-Market Considerations

The research findings indicate that brands need to understand that shopper is comparing more, switching more and making more deliberate choices. Naik believes a few adjustments are required:

- First, brands should lead with value, but not necessarily cheapness. The features can come through price, pack size, quality, convenience, health benefits, durability or trusted performance. Premium products can still work, but they need a stronger reason to exist.

- Second, brands should rethink price-pack architecture. A single mainstream pack may no longer serve all households. Brands need opening price points for budget-constrained shoppers, family-size or club-style value packs for stock-up missions, and premium formats only where the benefit is obvious.

- Third, promotions need to become smarter. Broad discounting can train shoppers to wait for deals and hurt margins. Brands should use retailer data to target promotions to switchers, lapsed buyers and high-potential households, while protecting baseline price integrity.

- Fourth, online channel should be taken more seriously. Consumers who shop online are doing so as a habit now, not just for convenience. That means investing more in retail media, search visibility and personalized promotions, because shoppers are increasingly making decisions before they even enter a store aisle.