How to Respond to High Grocery Prices

GROCERIES ACCOUNT for a significant portion of monthly spending in the US — as much as a third or more of discretionary income for a middle-to low-income family.

So, when the average grocery trip became 25% more expensive between 2020 and 2024, consumers certainly took notice. Of course, grocery prices became a hot national topic and a big part of the 2024 campaign. There was no shortage of ideas on lowering prices for everyday items, but they generally fell into price controls versus free market buckets.

The underlying factor driving price increases – inflation – is often discussed as the rate of change, which is one measure of the health of the current economy. Generally, we expect that rate of change to be around 2% for a healthy economy, with wages usually increasing slightly above that rate.

However, price inflation is cumulative over a period of time. The rate of increase we are seeing is off a higher base than the period before. When we hear that inflation has come down to 2.5%, that’s from its high of 9%. That doesn't mean prices have come down; it means prices continue to increase at a more reasonable pace.

Saturation Point

Manufacturers and retailers are realizing that a saturation point has been reached in many grocery categories. They know prices are beyond the consumer’s willingness to pay, but are struggling to find a clear plan for dealing with it.

While consumers want lower prices, the impact of the current environment is more likely to result in prices freezing rather than price declines.

You may ask why prices would freeze rather than fall. The primary arguments for this view are that input costs are still high, and packaging and energy costs are still higher than in previous years. The MAHA initiative will likely drive costs as manufacturers navigate federal and state-level regulations for a healthier food chain. So, while manufacturers and retailers are fueling growth through non-price levers like innovation, cost containment and efficiency improvements, margin erosion is still a challenge coming off a long period of inflation.

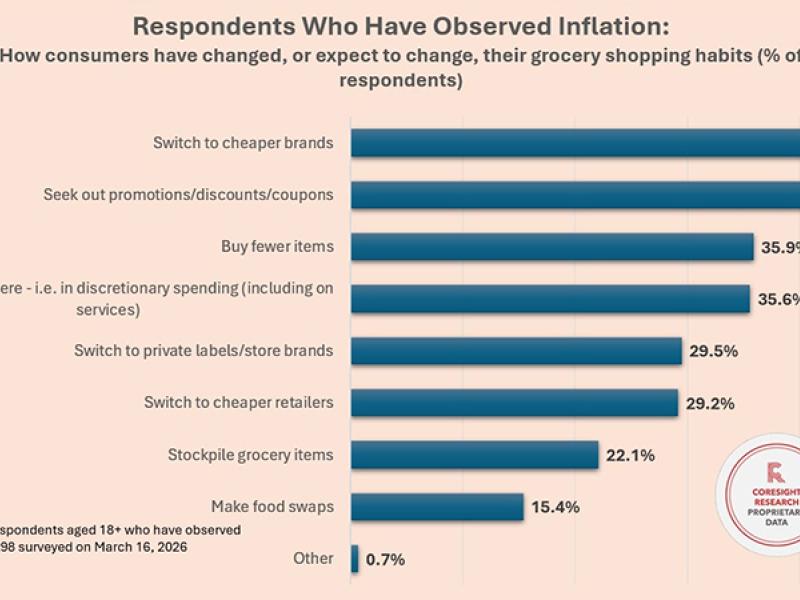

Shoppers are responding by trading down, comparing features, and deciding what really matters when buying everything from toothpaste to cereal to toilet paper. They are buying less and smaller sizes or making smaller overall purchases. They value essentials over premium items and embrace omnichannel to find the best price or deal.

Against this backdrop, private label is reaping the benefits. Consumers are finding that store brands have essentially “caught up” in quality, with some product categories, such as OTC drugstore brands, proving the case for many people.

Store brands are surging. During the pandemic, private label growth in groceries doubled that of national brands and expanded at 2-3% yearly. Retailers are counting on this to continue and are increasingly pushing their brands. Shoppers are more willing to try, mainly driven by price. However, product quality has improved, so consumers are more willing to stick with private labels than before.

How should brand manufacturers respond?

One, be really conscious of pricing. There are likely spots in your portfolio price architecture where margins have recovered. Assess which brands you might be able to take prices down on. While that is hard for a manufacturer to do, if there's a place where you have that opportunity, you can win over consumers by helping them save money and roll back the price. That is, providing that retailers don’t continue to price up, this takes an excellent sales story showing incremental value for the retailer, such as increased trips, larger basket size, etc.

Second, focus on innovation. Bring out new items, but tighten your innovation pipeline around the bigger ideas and focus on getting them out to market fast. It’s okay to fail small, so choose to pilot more often, leveraging AI to lower the cost of bringing new products to market. An innovative pipeline centered around driving value will become increasingly important when the price level alone is gone. Drive pricing and growth through innovation in features and functions.

Finally, when did you last look at your product’s pricing across each channel and align it with the consumer’s willingness to pay? Your consumers now do that across the omnichannel universe, where they shop daily.

So, if you have a discrepancy or a problem in your pricing strategy where you are out of line in one of the channels, shoppers are quickly picking up on that.

Shoppers’ expectations in various channels are different. They expect to pay more for convenience, but what is the limit? Online continues to grow, but what value does your customer attach to the in-store experience, and how does that translate to product markup? Manufacturers could be either leaving money on the table or leaking volume if they don’t realize a gap in pricing structure that consumers have noticed by shopping in different channels. Or if a shift in purchasing behavior hasn’t been reflected in your future omnichannel pricing strategy.

We are starting to see freight, fuel and general energy costs around production and manufacturing coming down, which will ultimately feed into P&L and make things cheaper to make. But in the short term, we are likely not going to see wide-scale price retraction. We're in for stabilization and a continuing shift toward private label.

Robert Baker is a Partner at Roland Berger, a global consultancy. For more information, visit www.RolandBerger.com