For CPG Brands, EPR Laws Rewrite the Economics of Packaging

AT FIRST GLANCE, that shampoo bottle or detergent jug may look the same. Still, behind the scenes, consumer brands are increasingly stripping out colored plastics, simplifying materials, and reworking as packaging systems as Extended Producer Responsibility (EPR) laws spread across the U.S.

What began as a policy shift intended to transfer recycling costs from municipalities to manufacturers is now reshaping how products are designed, packaged and marketed.

EPR laws – Oregon’s was the first to take effect in 2025 – require companies to fund the collection, recycling and disposal of the packaging they produce, tying costs directly to material choices and recyclability.

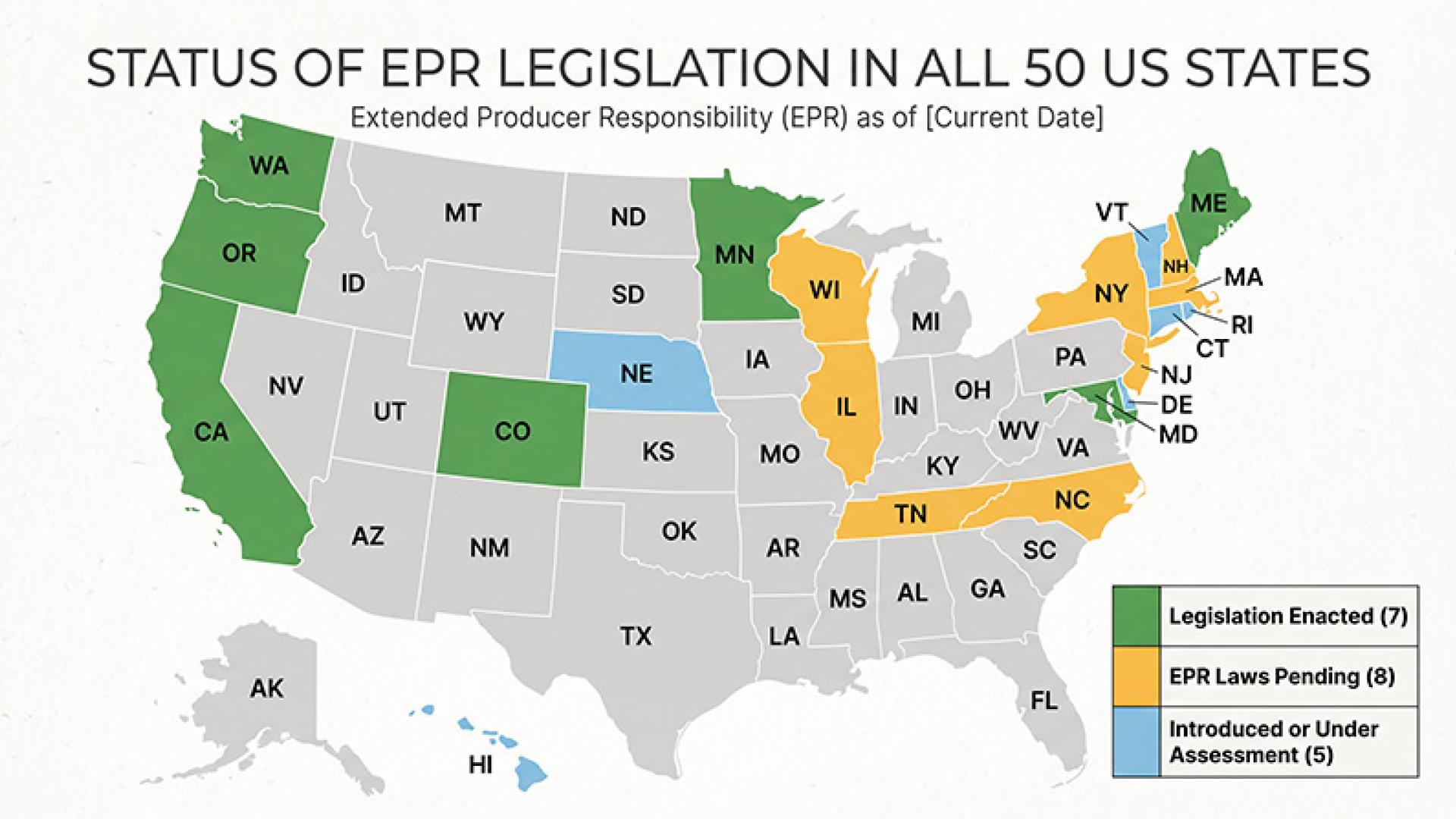

As of this writing, six additional states have enacted packaging EPR statutes with varying language and rules. New legislation has been introduced in eight more, and others are studying options:

- EPR Legislation Enacted (7): Maine, Oregon, Colorado, California, Minnesota, Maryland, Washington

- EPR Laws Pending (8): New York, New Jersey, Illinois, Massachusetts, New Hampshire, North Carolina, Tennessee, Wisconsin

- Introduced or Under Assessment (5): Hawaii, Rhode Island, Vermont, Nebraska, Connecticut

The wave of action across 22 states and counting presents a new form of complexity for CPG manufacturers, along with a fundamental shift in responsibility and a rethinking of materials and design. It is not viable to produce and distribute alternate packaging forms for different geographic regions.

The focus on sustainability compliance also means that packaging is now much more than just a vehicle for branding. It is a cost center. For CPGs, that shift is already translating into tangible changes, especially in the use of plastics.

Brand balancing acts

At Unilever, packaging teams are experimenting with refill systems, alternative materials and simplified formats designed to reduce waste and improve recyclability. The company has run more than 50 refill and reuse pilots globally and continues to invest in packaging redesign and recycled materials.

“Unilever is a long-time supporter of well-designed EPR policies,” Kristina Friedman, Head of Sustainability for Unilever North America, told CPGMatters. “We see them as critical tools for addressing plastic use and waste when they are fair, inclusive and hold businesses accountable for their packaging choices.

Citing the company’s long-term advocacy for EPR, Friedman said that they have been preparing for the implementation of these policies for years. “Across our portfolio, we’re focused on reducing our use of virgin plastic, increasing actual recyclability, and designing packaging for reuse and refill. For example, in 2025, we reduced our global virgin plastic footprint by 29% compared to 2019.”

In North America, Unilever has reached over 40% recycled plastic across its packaging footprint, and launched one of the first recyclable pumps for its Vaseline brand, she noted. “These types of innovations and initiatives help us meet our sustainability goals, create a more resilient business that’s prepared for EPR legislation implementation, and align with EPR frameworks that incentivize companies to design more sustainable packaging.”

The company has emphasized in sustainability communications that scaling reuse and refill models will require regulatory support and broader system change, reflecting the growing alignment between corporate strategy and emerging EPR frameworks.

Procter & Gamble is taking a complementary approach, investing in both material innovation and recycling infrastructure.

“We are working to reduce our use of virgin plastic and increase the use of recycled content,” said Jon Moeller, chairman of the board, president and chief executive officer of Procter & Gamble. “At the same time, we are investing in solutions to ensure more plastic is collected and recycled.”

The company has explored plant-based plastics and is investing in advanced recycling technologies capable of processing hard-to-recycle materials such as flexible and multi-layer packaging. Those formats are often penalized under EPR fee structures, making them a priority for redesign.

Luxury brings its own complexity

For premium players like Estée Lauder Companies, the transition is more complex. High-end beauty packaging has traditionally relied on mixed materials, intricate components and aesthetic finishes that can be difficult to recycle.

“We are increasing the use of recyclable, refillable and reusable packaging across our portfolio,” said Fabrizio Freda, executive chairman of The Estée Lauder Companies Inc. “At the same time, we must maintain the luxury experience consumers expect.”

That balancing act underscores how deeply EPR reaches into product design.

Those changes are not happening in isolation. They are increasingly shaped by consumer expectations as much as by regulation.

Research from Kantar shows that nearly 88% of consumers say reducing packaging is important to their purchasing decisions. At the same time, McKinsey & Company found that about half of U.S. consumers are willing to pay more for sustainable packaging, though most are only willing to pay a modest premium.

That creates both opportunity and risk. More than half of consumers say they have reduced or stopped buying brands due to environmental concerns, according to Kantar.

But it is also becoming one of the most scrutinized. Sustainable packaging is quickly shifting from a point of differentiation to a baseline expectation.

Packaging for ‘circularity’

That tension helps explain why policymakers are stepping in. Weak recycling infrastructure and inconsistent collection systems have long limited the effectiveness of voluntary corporate commitments. EPR advocates seek to close that gap by creating a more standardized, better-funded system, one in which producers have a direct financial incentive to design packaging that is easier and cheaper to recycle.

Not surprisingly, push-back has started in the courts. Of particular note is a constitutional challenge to the Oregon statute by the National Association of Wholesaler-Distributors (NAW). A preliminary injunction was granted by a U.S. District Court in February after the plaintiffs argued its rule discriminates against out-of-state suppliers.

For brands, the patchwork of incentive structures is already reshaping decision-making. Materials like colored PET plastics, multi-layer films and mixed substrates, long favored for durability or shelf appeal, are increasingly being phased out in favor of simpler, more recyclable alternatives such as clear plastics, paper-based packaging, aluminum and glass.

The shift also carries financial implications. Under EPR, companies pay fees based on the type and volume of packaging they place on the market, with less recyclable materials typically incurring higher costs. While estimates vary, the broader impact is clear. Packaging decisions now have direct, ongoing financial consequences that persist beyond the cost of production.

Industry groups are divided on how those costs will play out. The Consumer Brands Association has supported EPR frameworks in principle but cautioned that a patchwork of state laws could increase compliance complexity for manufacturers operating nationally. At the same time, organizations such as The Recycling Partnership argue that producer funding is critical to modernizing the U.S. recycling system and closing long-standing infrastructure gaps.

Ultimately, the biggest shift may be cultural. For decades, packaging was optimized for cost, convenience and shelf impact. Now, it is increasingly being designed for circularity.

The packaging may look the same, but how it is made, used and paid for is changing.